[ad_1]

The present wave of layoffs, a tough part of the innovation growth/bust cycle, differs from the earlier years’ dynamics.

B2B firms have decreased headcount to a larger extent than at any time since 2020.

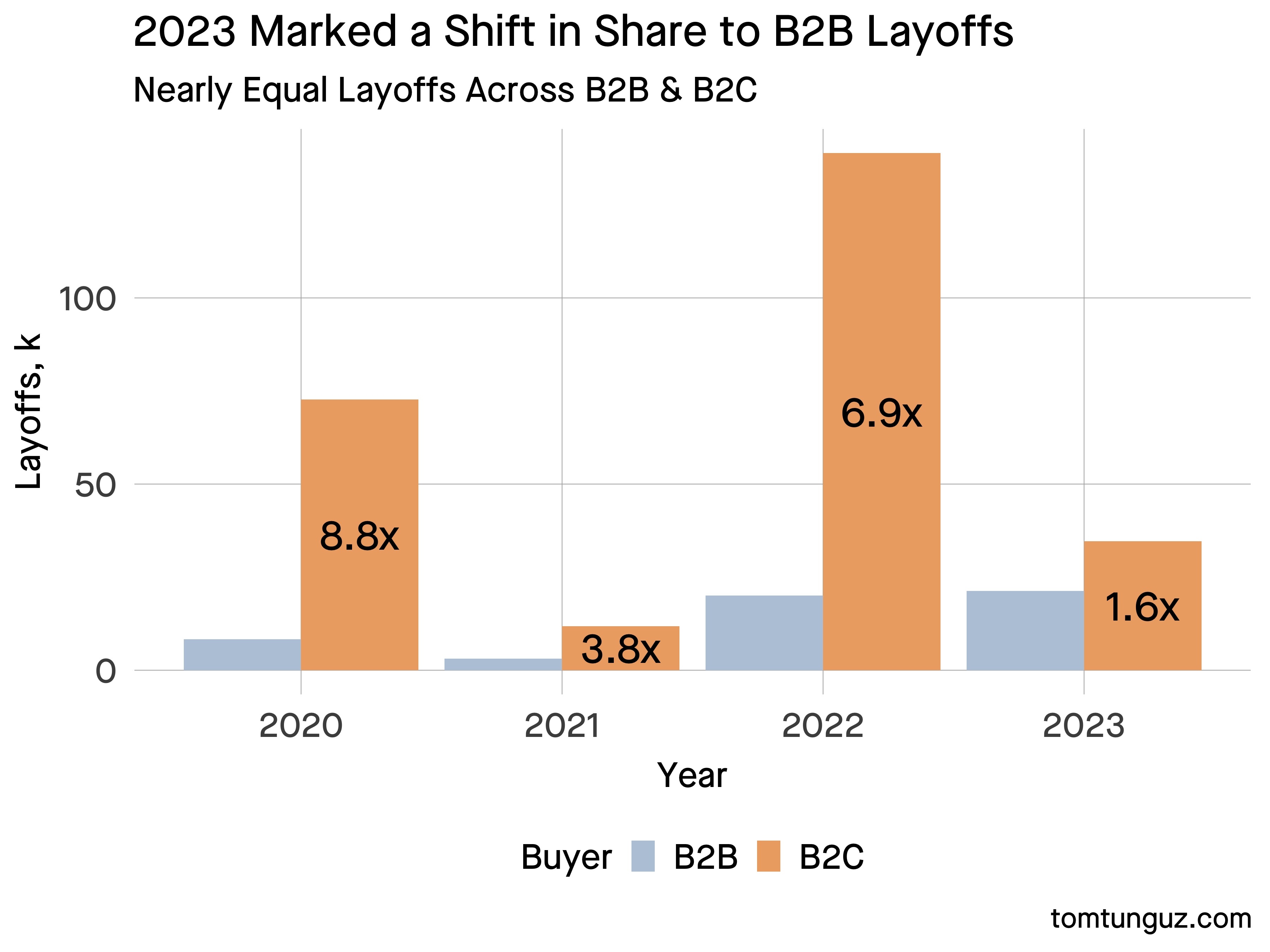

Within the final three years, B2C startups’ ratio of layoffs have dwarfed B2B layoffs. In 2020, B2C firms lower 8.8x the variety of B2B workers. 3.8x in 2021, & 6.9x in 2022.

12 months-to-date in 2023, the determine is 1.6x, simply 60% extra.

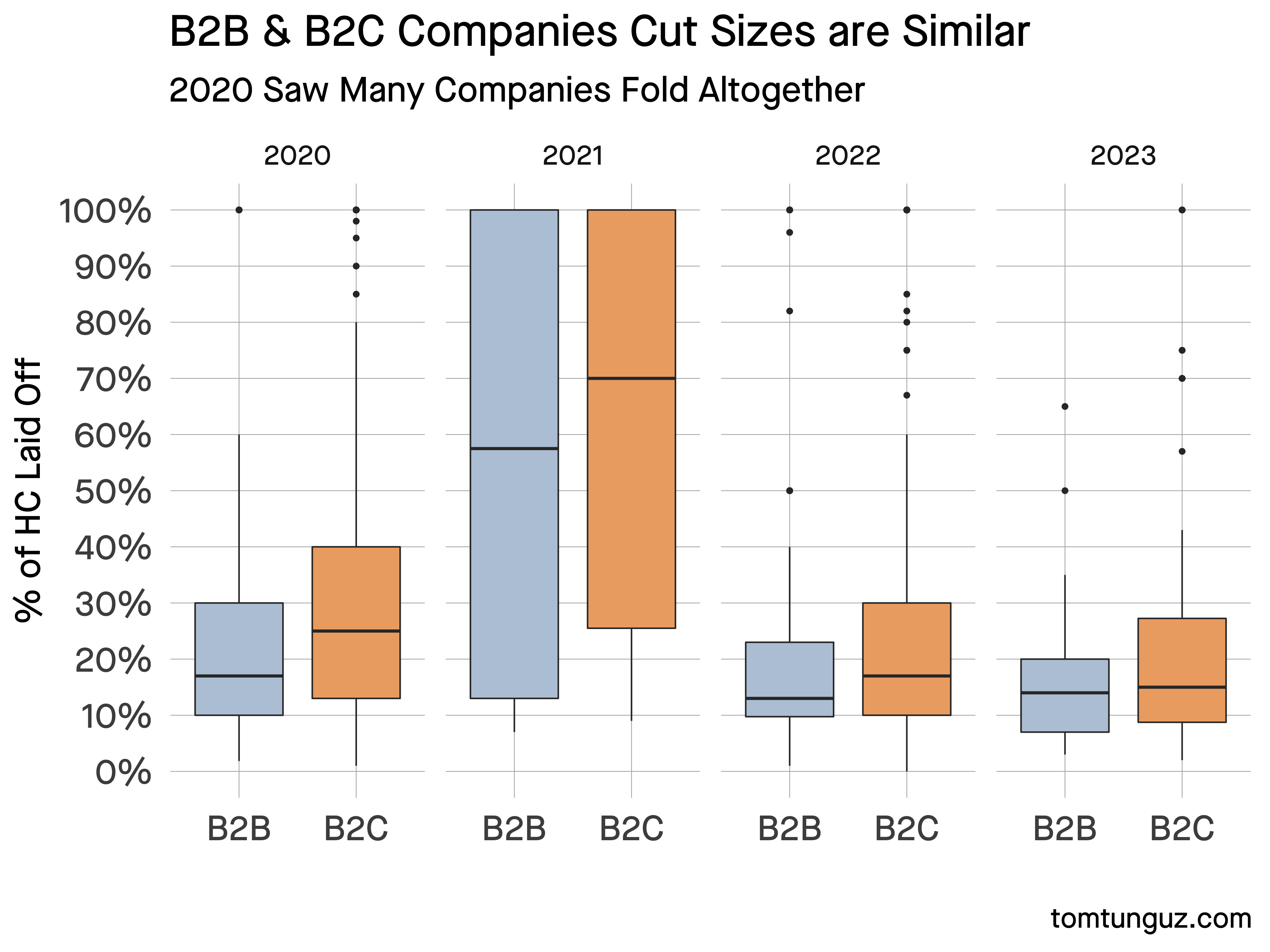

Discount magnitudes don’t differ by purchaser kind. B2B & B2C firms each downsize round 15% on common, with a seventy fifth percentile of 30%.

Tangentially, Covid impacted each segments. The typical layoff lower 50% or extra of workers & greater than 1 / 4 of those companies folded. However this can be a statistical aberration from a tiny variety of firms.

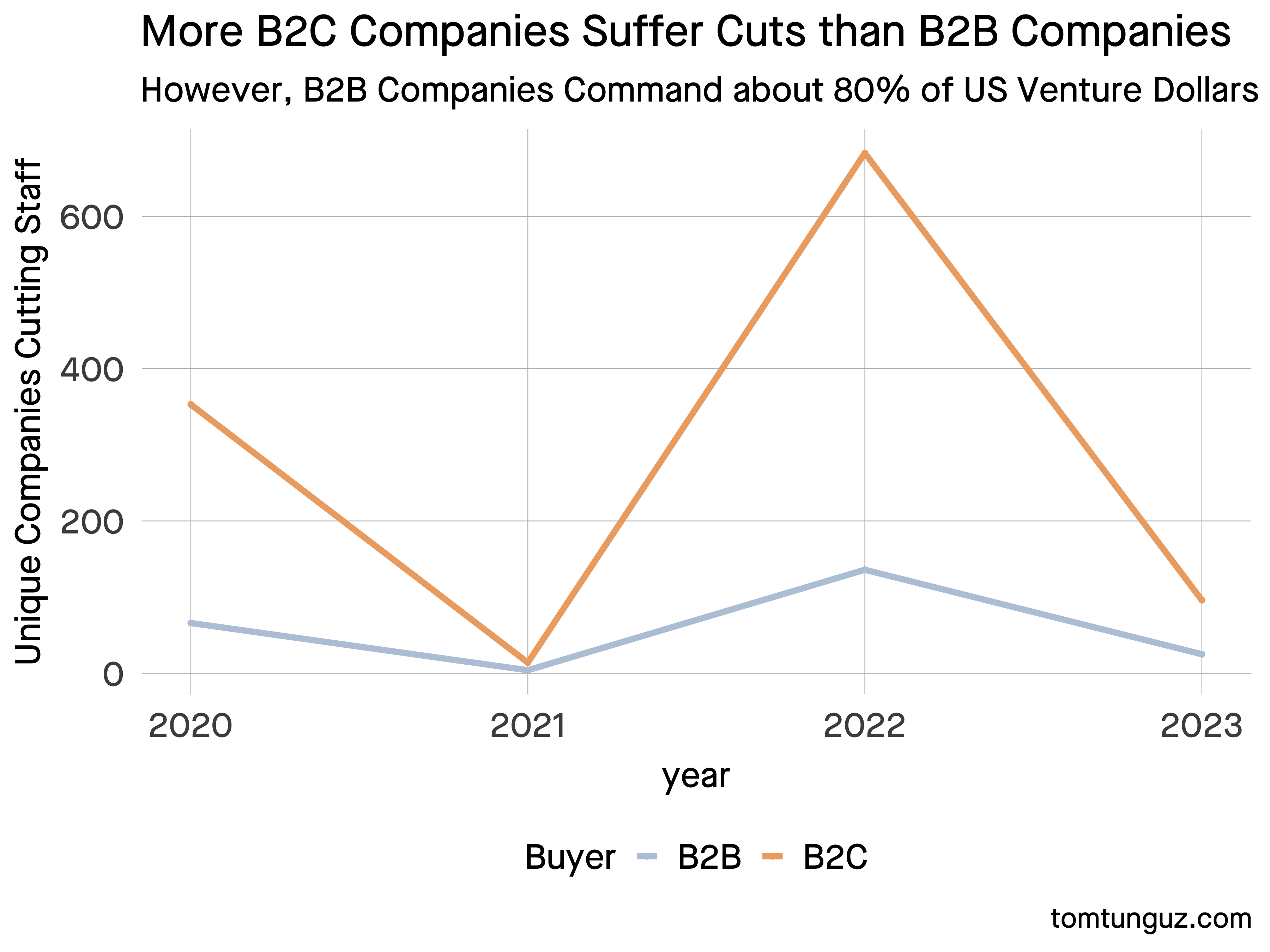

As a substitute, the gross variety of firms explains the delta between B2B/B2C layoffs. However this isn’t an endemic phenomenon.

| Information Level | B2B | B2C |

|---|---|---|

| Firms Raised Capital | 21,256 | 17,109 |

| Whole Raised, $b | 275 | 229 |

| Raised per Firm, $m | 77 | 75 |

About 4k fewer B2C firms than B2B firms raised roughly equal capital since 2020, which suggests B2C firms might endure from increased volatility basically: extra exploratory enterprise fashions, extra threat to their core companies when market circumstances change.

Longer-term contracts & steadier enterprise patrons assist clean shocks for B2B firms.

The principle challenges going through B2B startups as we speak are decreases in seat counts as their clients downsize & slower gross sales cycles which creates volatility in bookings, which has prompted extra layoffs than an anytime within the final 4 years.

[ad_2]